LOS ANGELES/SOUTH BAY - TRENDING NOW

The Los Angeles/Southbay industrial market includes major portions of Los Angeles County and the City of Long Beach. The area has long been one of the busiest industrial markets in the country, driven primarily by the Ports of Long Beach and Los Angeles, which together handle up to 40% of the nation’s cargo activity. In 2016, it was a record year for container volume at the Port of Los Angeles, despite the opening of the expanded Panama Canal, and conditions remain favorable for further gains in 2017. TEU volumes are expected to increase by as much as 4% to 5% in 2017. In Q1, the Port of Long Beach was up 1.5% and the Port of Los Angeles was up by over 10%. While big retailers account for a significant portion of the import value, many face significant challenges going forward. For many brands and suppliers, the 2017 holiday selling season could be a make it or break it year.

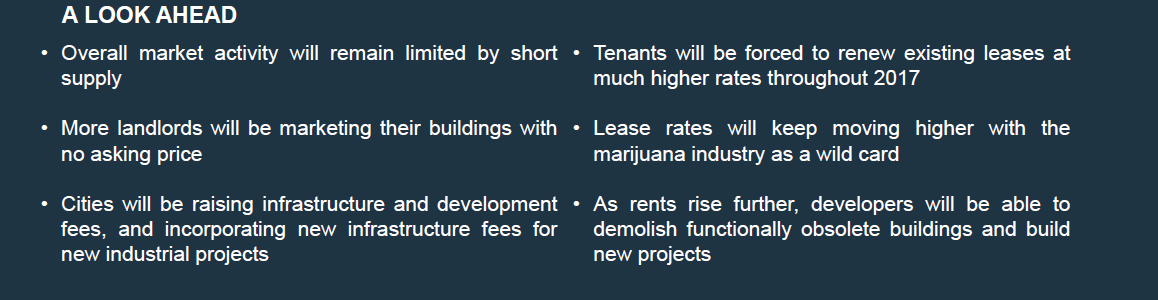

In Q1, there were a couple of disruptions to market conditions that impacted market dynamics. The first relates to the fact that several South Bay municipalities have legalized the cultivation and distribution of marijuana pursuant to the recent state referendum. Sales prices for buildings under 100,000 square feet in the City of Long Beach have spiked by 50% to 100%, literally overnight. The appetite the industry has for space is unprecedented, and building owners are taking advantage of the must-have nature of the requirements by demanding shorter escrows and non-refundable deposits on top of the inflated prices.

The second relates to a recent decision by the City of Carson to place a 45-day moratorium that affects all industrial developments, as well as any new lease or lease renewal for more than three years in term or in a building with more than five dock doors. City officials refer to the move as a “pause button” motivated by concerns over safety for the city’s residents.

The business community’s response to the move has been overwhelmingly negative for the city, which has long been known as business-friendly to logistics tenants, landlords and developers.

Manufacturing, value add distribution and self-fulfillment companies continue to experience greater demand as world economies tend to favor some component of domestic labor. These companies tend to have larger balance sheets and are willing to pay more for space than 3PL operators who don’t move their own product. While these companies tend to favor the Inland Empire for its larger buildings and labor pool, more of them are looking to infill locations around the South Bay.

Vacancy remained unchanged at just 1.1% in Q1. Distribution space is being absorbed almost immediately, often before hitting the open market. Landlords are celebrating when existing tenants with renewal options decide to move because it gives them a chance to assert their market advantage and push for longer lease terms, higher rents and stronger credit. As we remarked last quarter, it’s good to be king, but it may be even better to be a landlord in the South Bay these days.

The average asking rental rate moved up a penny to $.82/square foot/month. But, asking rates are becoming less of a market indicator because a substantial amount of space being offered for lease without a price. So, asking rents may not present a clear picture on actual rent growth. The final quarter of 2016 recorded net absorption of over 819,000 square feet, followed by a gain of 182,677 square feet in Q1. With vacancy so, net absorption becomes less of an indicator of market health.

Click here to read the full report.

The Los Angeles/Southbay industrial market includes major portions of Los Angeles County and the City of Long Beach. The area has long been one of the busiest industrial markets in the country, driven primarily by the Ports of Long Beach and Los Angeles, which together handle up to 40% of the nation’s cargo activity. In 2016, it was a record year for container volume at the Port of Los Angeles, despite the opening of the expanded Panama Canal, and conditions remain favorable for further gains in 2017. TEU volumes are expected to increase by as much as 4% to 5% in 2017. In Q1, the Port of Long Beach was up 1.5% and the Port of Los Angeles was up by over 10%. While big retailers account for a significant portion of the import value, many face significant challenges going forward. For many brands and suppliers, the 2017 holiday selling season could be a make it or break it year.

In Q1, there were a couple of disruptions to market conditions that impacted market dynamics. The first relates to the fact that several South Bay municipalities have legalized the cultivation and distribution of marijuana pursuant to the recent state referendum. Sales prices for buildings under 100,000 square feet in the City of Long Beach have spiked by 50% to 100%, literally overnight. The appetite the industry has for space is unprecedented, and building owners are taking advantage of the must-have nature of the requirements by demanding shorter escrows and non-refundable deposits on top of the inflated prices.

The second relates to a recent decision by the City of Carson to place a 45-day moratorium that affects all industrial developments, as well as any new lease or lease renewal for more than three years in term or in a building with more than five dock doors. City officials refer to the move as a “pause button” motivated by concerns over safety for the city’s residents.

The business community’s response to the move has been overwhelmingly negative for the city, which has long been known as business-friendly to logistics tenants, landlords and developers.

Manufacturing, value add distribution and self-fulfillment companies continue to experience greater demand as world economies tend to favor some component of domestic labor. These companies tend to have larger balance sheets and are willing to pay more for space than 3PL operators who don’t move their own product. While these companies tend to favor the Inland Empire for its larger buildings and labor pool, more of them are looking to infill locations around the South Bay.

Vacancy remained unchanged at just 1.1% in Q1. Distribution space is being absorbed almost immediately, often before hitting the open market. Landlords are celebrating when existing tenants with renewal options decide to move because it gives them a chance to assert their market advantage and push for longer lease terms, higher rents and stronger credit. As we remarked last quarter, it’s good to be king, but it may be even better to be a landlord in the South Bay these days.

The average asking rental rate moved up a penny to $.82/square foot/month. But, asking rates are becoming less of a market indicator because a substantial amount of space being offered for lease without a price. So, asking rents may not present a clear picture on actual rent growth. The final quarter of 2016 recorded net absorption of over 819,000 square feet, followed by a gain of 182,677 square feet in Q1. With vacancy so, net absorption becomes less of an indicator of market health.

Click here to read the full report.

RSS Feed

RSS Feed